Definition: The optimum equilibrium in supply and demand occurs when the quantity of a product that suppliers are willing to provide at a certain price matches the quantity that consumers are willing to buy at that price. In short, quantity supplied matches the quantity demanded at a particular price. This equilibrium point is where the supply and demand curves intersect.

Example: At the optimum equilibrium, both buyers and sellers are satisfied and benefited . Buyers are able to purchase the quantity they desire at a price they are willing to pay, mean while sellers are able to sell their goods or services at a price that covers their costs and provides a reasonable profit.

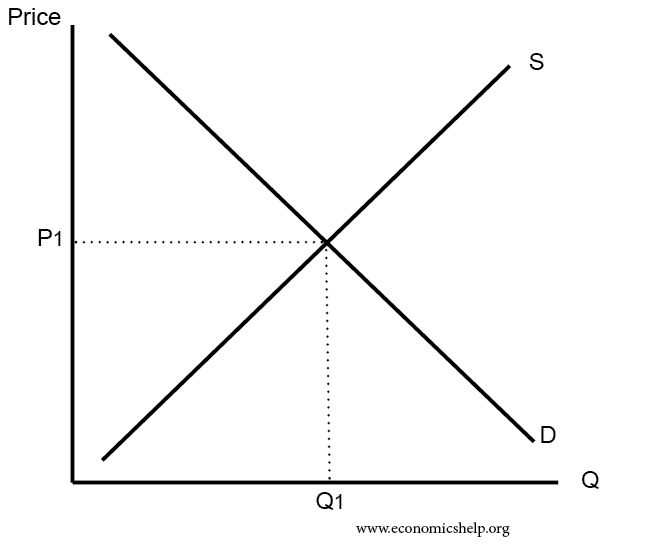

Graph eample:

The equilibrium price and quantity would be P1 and Q1